The Trusted Choice for Cash Loans

Request Your Cash Advance or Personal Loan Now

The Trusted Choice for Cash Loans

Submit your information today!

Get lender-approved in as fast as 5 min!

Receive a decision as soon as the next business day!

Fast Funding

Get money as soon as the next business day

How Digital Lending Platforms Work for Fast Funding

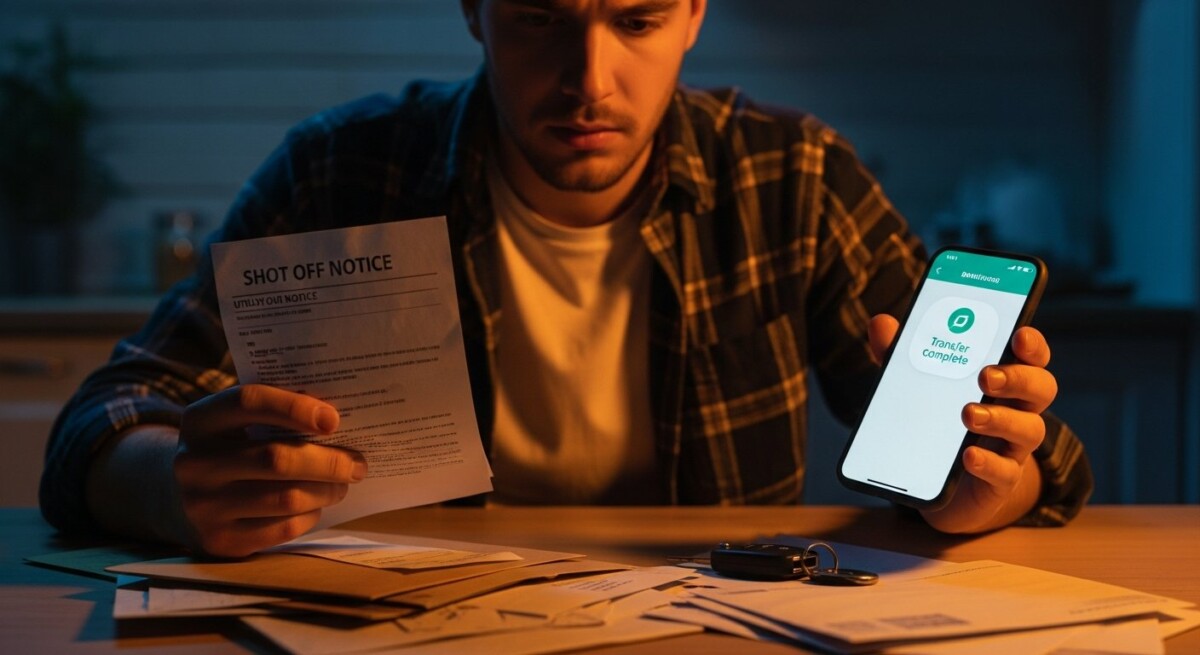

Imagine your car breaks down on a Tuesday morning. The repair shop quotes $800, and payday is still a week away. You start searching online for help, and that is when you discover how digital lending platforms work. These platforms connect people who need quick cash with lenders who can provide short-term solutions. Whether it is an urgent medical bill, a home repair, or a temporary cash shortage, digital lending offers a way to get funds without visiting a bank branch.

Understanding how digital lending platforms work

A digital lending platform is an online service that matches borrowers with potential lenders. Instead of walking into a bank or credit union, you fill out a simple form on a website. The platform then shares your information with a network of third-party lenders who review your request.

People typically consider this option when they need money fast and do not have time for traditional loan approvals. The process is designed for speed and convenience. You can complete the entire request from your phone or computer in minutes.

In simple terms, a digital lending platform acts as a middleman. It does not lend money directly. Instead, it streamlines the search for loan offers so you can compare terms and choose what works best for your situation. If a lender in the network approves your request, funds can often be deposited into your account as soon as the next business day.

When People Consider Short-Term Loans

Short-term loans are often a lifeline during unexpected financial emergencies. Life happens, and expenses do not always wait for your next paycheck. Many borrowers turn to these loans when they face a sudden gap between what they need and what they have available.

Common situations include:

- Unexpected bills like utility shut-off notices or insurance deductibles

- Urgent home repairs such as a broken water heater or roof leak

- Temporary cash shortages between paychecks

- Medical expenses for doctor visits, prescriptions, or emergency care

- Car repairs needed to get to work or school

These scenarios create real stress. Digital lending platforms offer a way to address the problem quickly, giving you time to focus on what matters most. However, it is important to remember that these loans are designed for short-term use and should not replace long-term financial planning.

If you are exploring short-term loan options, comparing lenders can help you find the right solution. Request loan offers or call to review available options.

Common Types of Short-Term Loans

Digital lending platforms offer several types of short-term loans. Each one has its own features, repayment structure, and typical use case. Knowing the difference helps you choose the option that matches your needs.

- Payday loans: Small-dollar loans meant to be repaid on your next payday. They are easy to qualify for but often carry high fees.

- Installment loans: Loans repaid in fixed monthly payments over several weeks or months. This structure can make budgeting more predictable.

- Personal cash advances: Short-term funds advanced against your upcoming income. Some platforms offer these as a line of credit.

- Online short-term loans: A broad category that includes any loan obtained through a digital platform with a repayment period of a few weeks to a few months.

Each type serves a different purpose. For example, an installment loan might work better for a larger expense like a car repair, while a payday loan could cover a smaller gap until payday. As you explore options, take time to understand the repayment schedule and total cost.

How the Loan Application Process Works

The application process on a digital lending platform is designed to be straightforward. You do not need to gather stacks of paperwork or wait in line. Most steps happen online with minimal hassle.

- Submit a loan request: Fill out a secure online form with basic personal and financial details, such as your name, income, and banking information.

- Provide income details: Lenders need to verify that you have a steady source of income to repay the loan. This may include employment or benefits information.

- Lender review and approval: The platform sends your request to multiple lenders in its network. Each lender reviews it independently and decides whether to make an offer.

- Receive loan offers: If approved, you will see offers that include the loan amount, interest rate, fees, and repayment terms. You can compare them side by side.

- Receive funds if approved: Once you accept an offer and complete any final verification, funds are typically deposited directly into your bank account, often by the next business day.

This process can take as little as a few hours from start to finish. The speed depends on the lender and the time of day you submit your request. For a deeper dive into a similar model, our guide on how peer-to-peer lending platforms work explains how individual investors fund loans in a comparable online environment.

Comparing multiple lenders can help you find loan terms that match your situation. Compare loan offers or call to explore available funding options.

Factors Lenders May Consider

Lenders on digital platforms do not all use the same criteria, but most review a few key factors to decide whether to approve your request. Understanding these can help you prepare and improve your chances.

- Income verification: Lenders want to see that you have a regular source of income, whether from a job, self-employment, or benefits.

- Employment status: Stable employment often signals that you can repay the loan on time.

- Credit history: Some lenders check your credit score, but many short-term lenders accept borrowers with less-than-perfect credit.

- Repayment ability: Lenders assess whether your income is sufficient to cover the loan payment along with your other expenses.

If you have bad credit, do not assume you are automatically disqualified. Many digital lending platforms work with lenders who specialize in helping borrowers with a range of credit profiles. The key is to be honest about your income and expenses so you receive offers you can realistically afford.

Understanding Loan Costs and Terms

Before accepting any loan offer, take time to understand the total cost. Short-term loans often come with higher interest rates than traditional bank loans because they are unsecured and designed for fast access.

Interest rates are typically expressed as an Annual Percentage Rate (APR), which includes both the interest and any fees. Repayment periods can range from a few weeks to several months. Some loans also include origination fees, late payment penalties, or prepayment penalties if you pay off the loan early.

Always read the fine print. Ask yourself: Can I afford the payment on my next payday? What happens if I am late? Knowing these details upfront helps you avoid surprises. If an offer seems confusing, ask the lender for clarification or look for a different option. Responsible borrowing starts with understanding exactly what you are agreeing to.

Loan terms can vary between lenders. Check available loan offers or call to review possible options.

Tips for Choosing the Right Loan Option

Finding the right loan is about more than just getting approved. You want a loan that fits your budget and helps you solve your financial problem without creating new ones. Use these tips to make a smart choice.

- Review repayment terms carefully: Look at the due date, payment amount, and total cost. Make sure you can repay on time.

- Compare multiple lenders: Do not accept the first offer you receive. Different lenders may offer different rates and terms for the same loan amount.

- Borrow only what is needed: It can be tempting to take a larger loan, but borrowing more than necessary increases your cost and repayment risk.

- Plan repayment in advance: Set a reminder for the due date and budget for the payment. Consider automatic payments if available.

Taking these steps helps you avoid common pitfalls like rollovers or late fees. Remember, a loan is a tool,use it carefully to meet your immediate need without straining your finances further. For more insight into how different lending models compare, read our article on how peer-to-peer lending platforms work for borrowers to see another option for obtaining funds online.

Responsible Borrowing and Financial Planning

Short-term loans can provide relief during a tough moment, but they work best as part of a larger financial plan. Responsible borrowing means using credit only when necessary and repaying it as agreed.

Start by creating a simple budget that tracks your income and expenses. Knowing where your money goes each month helps you identify areas where you can save. If you use a short-term loan, include the repayment in your budget immediately so it does not slip through the cracks.

Avoid the cycle of borrowing repeatedly to cover everyday expenses. If you find yourself needing loans frequently, consider reaching out to a nonprofit credit counselor or exploring other resources. Digital lending platforms are a bridge, not a permanent solution. Using them wisely protects your credit and your peace of mind.

What credit score do I need for a digital lending platform loan?

Many digital lending platforms work with lenders who accept borrowers with various credit scores, including those with bad credit or no credit history. While some lenders do check credit, others focus more on your income and ability to repay. You do not always need a high score to get approved.

How fast can I get money from a digital lending platform?

If you submit your request early in the day and get approved, funds can often be deposited into your bank account by the next business day. Some lenders offer same-day funding for requests submitted before a certain cutoff time. Speed varies by lender and your bank’s processing times.

Are digital lending platforms safe to use?

Reputable platforms use encryption and secure technology to protect your personal and financial information. Always check that the website uses HTTPS and read the privacy policy before submitting your details. Express Cash, for example, takes data security seriously and partners only with licensed lenders.

Can I use a digital lending platform if I am self-employed?

Yes, self-employed borrowers can typically apply. You will need to provide proof of income, such as bank statements or tax returns, to show that you have a steady cash flow. Lenders want to see that you can repay the loan regardless of your employment type.

What happens if I cannot repay my loan on time?

If you cannot repay on time, contact your lender immediately. Some lenders offer extensions or payment plans, but these may come with additional fees. Ignoring the due date can lead to late penalties, additional interest, and potential damage to your credit score. Communication is key.

Do digital lending platforms charge fees to submit a request?

Most platforms, including Express Cash, do not charge you any fees for submitting a loan request. The service is free for borrowers. If a lender approves your request, any applicable fees will be disclosed in the loan offer before you accept.

How much can I borrow through a digital lending platform?

Loan amounts vary by lender and your state of residence. Short-term loans typically range from $100 to $5,000. The amount you qualify for depends on factors like your income, repayment ability, and state regulations. Borrow only what you need to cover your expense.

Will a short-term loan affect my credit score?

Some lenders report your payment activity to credit bureaus. Making on-time payments can help build or improve your credit history. Missing payments may have a negative impact. Before you apply, ask the lender whether they report to the major credit bureaus.

Choosing the right financial solution starts with understanding your options. Whether you need funds for an emergency expense or a temporary gap, take the time to compare lenders, review terms carefully, and borrow responsibly. Digital lending platforms offer a fast and convenient way to access short-term funding when used wisely. Explore available offers, ask questions, and select the loan that best fits your needs and budget. Learn more

About Mia Turner

Related Posts