The Trusted Choice for Cash Loans

Request Your Cash Advance or Personal Loan Now

The Trusted Choice for Cash Loans

Submit your information today!

Get lender-approved in as fast as 5 min!

Receive a decision as soon as the next business day!

Fast Funding

Get money as soon as the next business day

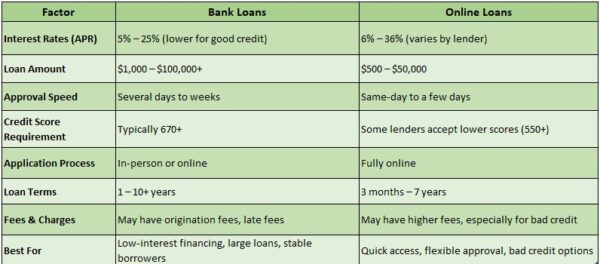

Bank Loan Rates vs. Online Loan Rates: Which Is Cheaper?

Understanding Bank Loan Rates and Their Impact on Borrowing Costs

Understanding the differences between Bank loan rates vs. Online loan rates is crucial for managing borrowing costs. Traditional banks have established reputations and offer a variety of services, but their loan rates can be higher due to overhead expenses. In contrast, online lenders often operate with lower costs, resulting in more competitive rates. However, it’s important to consider various factors beyond just the rates when choosing where to borrow. Here are some key points to consider when comparing bank loan rates to online loan rates:

- Interest Rates: Online lenders frequently provide lower interest rates, particularly for personal and small business loans, leading to significant savings over time.

- Fees: Banks may impose higher processing fees, while many online lenders offer clearer fee structures with fewer hidden charges.

- Approval Times: Online loans typically have quicker approval processes, allowing for faster access to funds when needed.

- Customer Service: While banks may provide in-person assistance, online lenders often excel in customer service through chat and phone support, making it easier to get help.

Ultimately, the decision between bank loan rates and online loan rates should be based on your financial situation and preferences. By carefully weighing these factors, you can make an informed choice that suits your borrowing needs.

Looking for fast and reliable personal loans? Visit ExpressCash to get started today!

When it comes to securing a loan, many borrowers find themselves weighing the options between traditional bank loan rates and online loan rates. This decision can significantly impact your financial future, so it’s essential to understand the nuances of each. Online lenders have surged in popularity, often touting lower rates and faster approval times. But are they genuinely more affordable? Let’s dive into the details. One of the primary advantages of online loan rates is their competitive pricing. Online lenders typically have lower overhead costs compared to brick-and-mortar banks, allowing them to pass those savings onto borrowers. Here are some benefits of choosing online loans:

- Lower interest rates: Many online lenders offer rates that can be significantly lower than traditional banks.

- Faster processing: Online applications can often be completed in minutes, with funds disbursed quickly.

- Flexible terms: Many online lenders provide a variety of repayment options to suit different financial situations.

However, it’s crucial to consider the potential downsides. While online loans may seem cheaper upfront, they can come with hidden fees or less favorable terms. Always read the fine print and compare offers from multiple lenders. In many cases, the best approach is to evaluate both bank loan rates and online loan rates side by side, ensuring you choose the option that best fits your financial needs.

Comparing Interest Rates: Bank Loan Rates vs. Online Loan Rates

When borrowing money, knowing the differences between bank loan rates and online loan rates can lead to significant savings. Traditional banks are often seen as stable, but they do not always offer the best rates. Online lenders have become popular for their competitive pricing and quicker application processes. So, which is cheaper? Let’s explore.

Bank Loan Rates: Bank loans typically feature fixed interest rates ranging from 3 to 10 percent, influenced by your credit score and loan type. The application process is usually more extensive, requiring credit checks and income verification. However, banks provide benefits like personalized service and the chance to build long-term relationships.

Online Loan Rates: Online lenders often present more flexible options, with rates as low as 2.5 percent for borrowers with excellent credit. Their application process is generally faster, with funds available in as little as 24 hours. However, be wary of hidden fees and potential variable rates that may rise over time. In summary, while bank loan rates offer stability and personalized service, online loan rates frequently provide better pricing and convenience. Consider these key points:

- Speed: Online loans are processed faster.

- Flexibility: Online lenders offer varied loan amounts and terms.

- Customer Service: Banks may provide more personalized support.

- Interest Rates: Online loans can have lower rates for good credit borrowers.

Ultimately, the best choice depends on your financial situation and preferences, so always compare rates and terms before deciding.

Need cash for unexpected expenses? ExpressCash offers quick and easy personal loans tailored to your needs.

The Role of Credit Scores in Bank and Online Loan Rates

Understanding the differences between bank loan rates and online loan rates often hinges on one key factor: your credit score. This score serves as a financial report card, significantly influencing how lenders view your creditworthiness. Generally, a higher credit score leads to lower interest rates, whether you are borrowing from a traditional bank or an online lender. If you maintain a solid credit history, you can enjoy better rates across the board.

For example, with a credit score of 750, a bank might offer a loan at 4 percent, while an online lender could provide a slightly lower rate of 3.5 percent. Conversely, if your score drops to 620, those rates could rise sharply, with banks potentially charging 6 percent and online lenders around 5.5 percent. This clearly shows how your credit score affects your borrowing options. Here are some essential insights to keep in mind when evaluating loan rates based on your credit score:

- Higher Scores Equal Better Rates: A better credit score increases your chances of securing lower interest rates.

- Shop Around: Always compare rates from both banks and online lenders to find the best deal.

- Consider Fees: Online loans may have lower rates but could come with higher fees, so read the fine print.

- Credit Score Monitoring: Regularly check your credit score to understand its impact on your loan options.

Hidden Fees: What to Watch Out for in Bank and Online Loans

When comparing Bank Loan Rates and Online Loan Rates, it’s crucial to consider more than just the interest rates. Hidden fees can significantly affect your total loan cost, making an attractive loan much pricier over time. Here are some common hidden fees to watch for:

- Origination Fees: Many lenders charge a fee for processing your loan application, typically ranging from one to five percent of the loan amount. Always inquire if this fee is negotiable.

- Prepayment Penalties: Some loans impose penalties for early repayment, which can be problematic if you plan to refinance or pay off your loan sooner than expected.

- Late Payment Fees: Be aware of the penalties for late payments, as these can accumulate quickly and increase your overall loan cost.

- Closing Costs: While more common with mortgages, some personal loans may also include closing costs that can surprise borrowers.

To make an informed choice, always read the fine print and ask your lender to clarify any unclear fees. For example, a bank with a lower interest rate but high origination fees might ultimately cost you more than an online lender with a slightly higher rate but fewer fees. The goal is to find the best overall deal, not just the lowest rate.

How Loan Terms Affect Bank Loan Rates and Online Loan Rates

When comparing bank loan rates and online loan rates, it’s essential to consider how loan terms influence overall costs. Typically, bank loans offer traditional terms that can result in lower interest rates, particularly for borrowers with strong credit. Conversely, online lenders provide more flexible terms, which can be appealing but may come with higher rates. Understanding these differences is crucial for making an informed decision about which option is cheaper for your needs.

For example, if you seek a personal loan of ten thousand dollars, a bank might offer a fixed rate of six percent for a five-year term, while an online lender might present an eight percent rate for a shorter repayment period. Although the bank loan seems cheaper, the flexibility of the online loan—like quicker approval and fewer requirements—might make it worth considering. Here are some key points to keep in mind:

- Loan Amount: Larger loans typically have lower rates at banks due to reduced risk.

- Credit Score: A higher score can unlock better rates at both banks and online lenders.

- Repayment Terms: Shorter terms usually mean higher monthly payments but less interest paid overall.

- Fees: Always check for hidden fees that can affect the total loan cost.

In conclusion, while bank loan rates may initially seem more attractive, online loan rates can offer advantages that might save you money in the long run. Your financial situation and preferred terms will ultimately guide your choice.

Customer Service and Support: Bank Loans vs. Online Loan Options

Choosing between bank loans and online loan options often hinges on customer service and support. While both lenders aim to assist borrowers, their methods can vary significantly. Traditional banks offer established reputations and face-to-face interactions, which can be reassuring for some. In contrast, online lenders excel in convenience and speed, providing support through chat, email, or phone without requiring in-person visits. Consider these key points when evaluating customer service for bank loans versus online loans:

- Accessibility: Online lenders generally provide 24/7 support, ensuring you can get answers whenever needed. Banks, however, may have limited hours, which can be inconvenient for urgent inquiries.

- Response Time: Online lenders often boast quick responses, sometimes offering instant approvals. Banks may take longer due to traditional processes, which can be frustrating if you need a loan quickly.

- Personal Touch: For those who value personal interaction, banks can offer face-to-face meetings with loan officers. Online lenders may lack this personal touch but compensate with user-friendly platforms and resources.

Ultimately, your choice between bank loan rates and online loan rates may depend on the level of customer service you prioritize. Understanding these differences can guide you in making an informed decision.

Making the Right Choice: Factors to Consider Between Bank and Online Loans

Choosing between bank loan rates and online loan rates requires careful consideration of your options. Each has its unique advantages, and understanding these can lead to a better decision. Traditional banks often offer lower interest rates for those with excellent credit, but they may impose stricter eligibility criteria and longer processing times. In contrast, online lenders provide a more streamlined application process and quicker approvals, which can be crucial if you need funds urgently. When comparing bank and online loan rates, consider these key factors:

- Interest Rates: Online lenders might have higher rates but serve a wider range of credit scores.

- Fees: Be aware of origination fees or prepayment penalties that can impact the total loan cost.

- Customer Service: Banks typically offer in-person support, while online lenders assist via chat or phone.

- Loan Amounts: Banks may require higher minimum loan amounts, which could limit options for smaller needs.

Ultimately, your choice should align with your financial situation and preferences. If you prefer personal interaction and potentially lower rates, a bank loan could be ideal. However, if speed and convenience are more important, online loans may be the better option. Comparing offers from both types of lenders and asking questions can help you make an informed decision, saving you money and reducing stress.

FAQs

-

How do bank loan rates compare to online loan rates?

Banks typically offer lower interest rates than online lenders, but online loans may have faster approval and more flexible requirements. -

Why are online loan rates often higher than bank loans?

Online lenders take on more risk by lending to borrowers with lower credit scores or limited financial history, leading to higher rates. -

Which type of loan is easier to qualify for—bank or online?

Online loans usually have more lenient credit and income requirements, while banks prefer borrowers with strong credit and financial stability. -

Do online loans have hidden fees compared to bank loans?

Some online lenders charge origination fees, higher late fees, or prepayment penalties, so always review the terms carefully. -

Which option is better for emergency borrowing?

Online loans provide quicker approval and funding, while bank loans may take longer but offer lower rates and better terms for qualified borrowers.

Don’t wait! Apply for a personal loan through ExpressCash and get the funds you need fast.

🔗Explore our website, AdvanceCash, to apply for a loan, or contact our customer service team today to learn more about how we can assist you.

About Ethan Davis

Related Posts